What Goes Up... Must Go Higher?

Rolling the Dice on “The Biggest Bubble Since the Railroads.”

by Richard Bavetz, ChFC®, CLU®, FRC℠

June 13, 2026

In the spring of 2026, the surface of the financial markets still looked remarkably intact. Stock indices keep bumping up the all-time highs in the S&P 500 and NASDAQ on the back of artificial-intelligence enthusiasm. Corporate earnings reports continue to beat lowered expectations in many sectors and the familiar chorus of “resilience” echoes from Wall Street strategists and cable-news pundits alike. Yet anyone who has spent the last three decades living through the boom-and-bust cycles while advising high-net-worth clients, endowments, and even families wanting sound advice, knows that the real story is rarely written on a page one headline. It is whispered in the quieter corners where liquidity assumptions meet economic reality, where floating-rate structures collide with sticky inflation, and where redemption queues begin to lengthen while underlying assets refuse to move at par.

It has been called “the Lowest Quality Asset Class across the leveraged finance universe,” by Bank of America’s Credit Strategy Team. What we are witnessing in Private Credit right now is not a headline-grabbing panic. It is something more insidious: a slow-motion recalibration that has been building since the second half of 2025 and is accelerating in real time through the first half of 2026. The events—gated redemptions, portfolio markdowns, dividend cuts at Business-Development Companies (BDCs), valuation disputes under regulatory scrutiny, and rescue capital injections—are being reported one-by-one and often framed as isolated “idiosyncratic” issues. That framing downplays the larger pattern. The indicators are pointing unmistakably toward a bubble that has inflated beyond sustainable levels, one that carries elements of both the late-1990s dot-com overvaluation in technology leverage and the 2008-era hidden credit contagion that ultimately washed back onto bank balance sheets.

This is not a call to liquidate everything tomorrow. It is a sober advisory from someone who has sat across the table from high-net worth investors or people simply wanting to retire for more than twenty-five years. The average person should be very concerned about their investments and the potential spillover into the banking sector that Private Credit poses. The evidence accumulating since late 2025 suggests we are facing a hybrid scenario: the speculative froth of dot-com-era optimism about transformative technology (this time centered on AI data centers and software) meeting the structural leverage and opacity problems that defined 2008’s credit crisis. Private credit, once touted as a diversifier that moved risk off bank balance sheets, is now revealing itself as a transmission mechanism that can move stress back into the system—through layered financing, redemption pressure, and even exposure in retirement accounts of all places, that could easily be described as “Mission-Creep.”

Markets don’t simply move up-or-down like an elevator. They are river systems. The volume of capital committed and the velocity with which that capital seeks to exit or enter determine whether the channel stays navigable or overflows its banks. Right now, the volume in private credit is enormous—well over $3 trillion in direct lending alone as some estimates show—and the velocity is shifting from inflow to outflow faster than many models anticipated. What goes up can indeed go higher for longer, even more than anyone expected. But when the flow reverses, the physics of velocity can turn dangerous and with remarkable speed.

Let’s walk through the mechanics in plain language, draw the connections that the daily headlines often miss, and offer practical guidance for anyone with exposure—direct or indirect—to this little-known asset class called Private Credit. We will examine the timeline of events, the interest-rate environment that has become a perfect storm, the role of Federal Reserve Chair Kevin Warsh, the opaque “mission creep” into pensions and 401(k)s, and how stress in private credit can propagate into broader markets and banking channels. Our focus remains on economic fundamentals. Extreme caution is warranted. Preparation is essential.

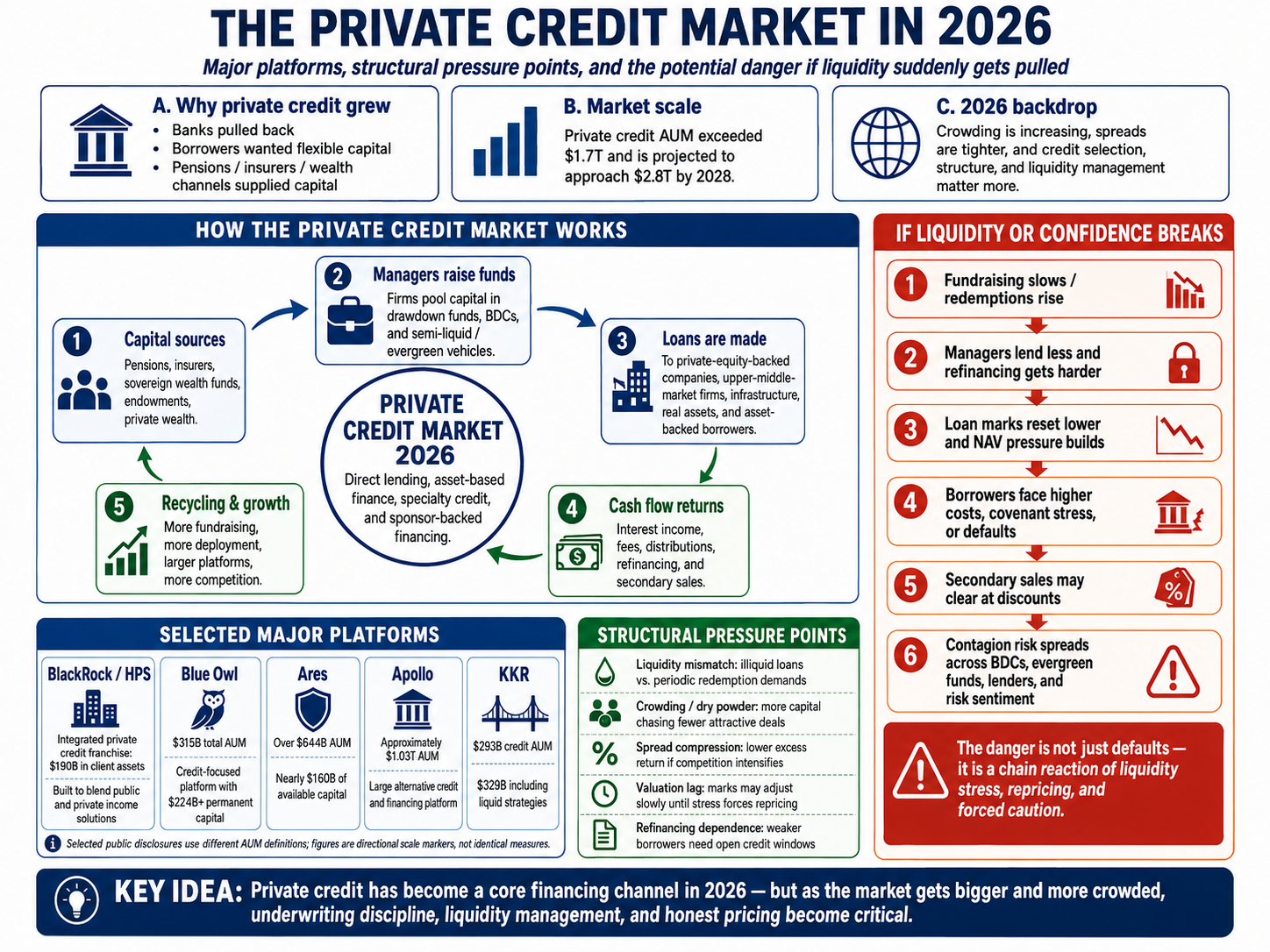

The Private Credit Landscape: Promise, Structure, and the Liquidity Mismatch

Private credit emerged in earnest after the 2008 crisis as banks pulled back from middle-market lending under stricter capital requirements. Non-bank lenders—firms like Blackstone, Apollo, KKR, Ares, Blue Owl, and others—stepped in, originating senior secured loans to companies that traditional banks no longer wanted to hold on their balance sheets. The structure was compelling on paper: floating rates tied to the Secured Overnight Financing Rate (SOFR) or similar benchmarks plus spreads of 500–700 basis points (5-7%), senior claims in the capital stack, and covenants designed to protect lenders. Investors, starving for yields in the zero-rate era, poured capital in. Funds promised quarterly or annual liquidity windows that seemed reasonable when inflows were strong and defaults low.

The appeal was straightforward. In a higher-rate environment, floating coupons were supposed to act as a natural hedge. Many managers and investors built their underwriting models around the assumption that if rates climbed too far or too fast, the Fed would eventually cut aggressively, easing debt-service burdens and allow refinancing on favorable terms. That assumption sat at the core of thousands of deals originated between 2020 and 2024. It still underpins much of the legacy book today.

What was underappreciated—and is now becoming painfully visible—is the embedded liquidity mismatch. Private-credit funds, especially newer semi-liquid or retail-access vehicles sold through wealth platforms, offer redemption rights far more frequently than the underlying loans' multi-year duration. In calm markets, managers can meet redemptions by drawing on unfunded commitments or selling higher-quality assets. When requests spike simultaneously across the industry, the choices narrow: managers must gate withdrawals, sell at discounts that crystallize losses, restructure loans with payment-in-kind (PIK) toggles, or charge off non-performing debt. Each path carries second-order effects that can ripple outward.

By and large, the low-rate environment that created Private Credit has now reversed, rates are still elevated and rising higher, refinancing has become harder, and the first real signs of stress are emerging across the asset class.

By the second half of 2025, the first cracks were already appearing. On December 17, 2025, major private-credit players began rethinking large commitments to AI data-center financing. The off-balance-sheet lease obligations of Hyperscalers such as Oracle were coming under fresh scrutiny. What had looked like bulletproof collateral in a low-rate, high-growth narrative suddenly appeared less certain when power costs, utilization rates, and capital-expenditure realities collided with elevated borrowing costs. Blue Owl was among the first to signal hesitation, but industry insiders understood it was not alone. The realization was dawning that the AI investment orgy carried layers of leverage that might prove unsustainable if economic growth or rate relief didn’t pan out.

Rug Pull: Rising Private Credit Defaults and the Hunt for Bag Holders

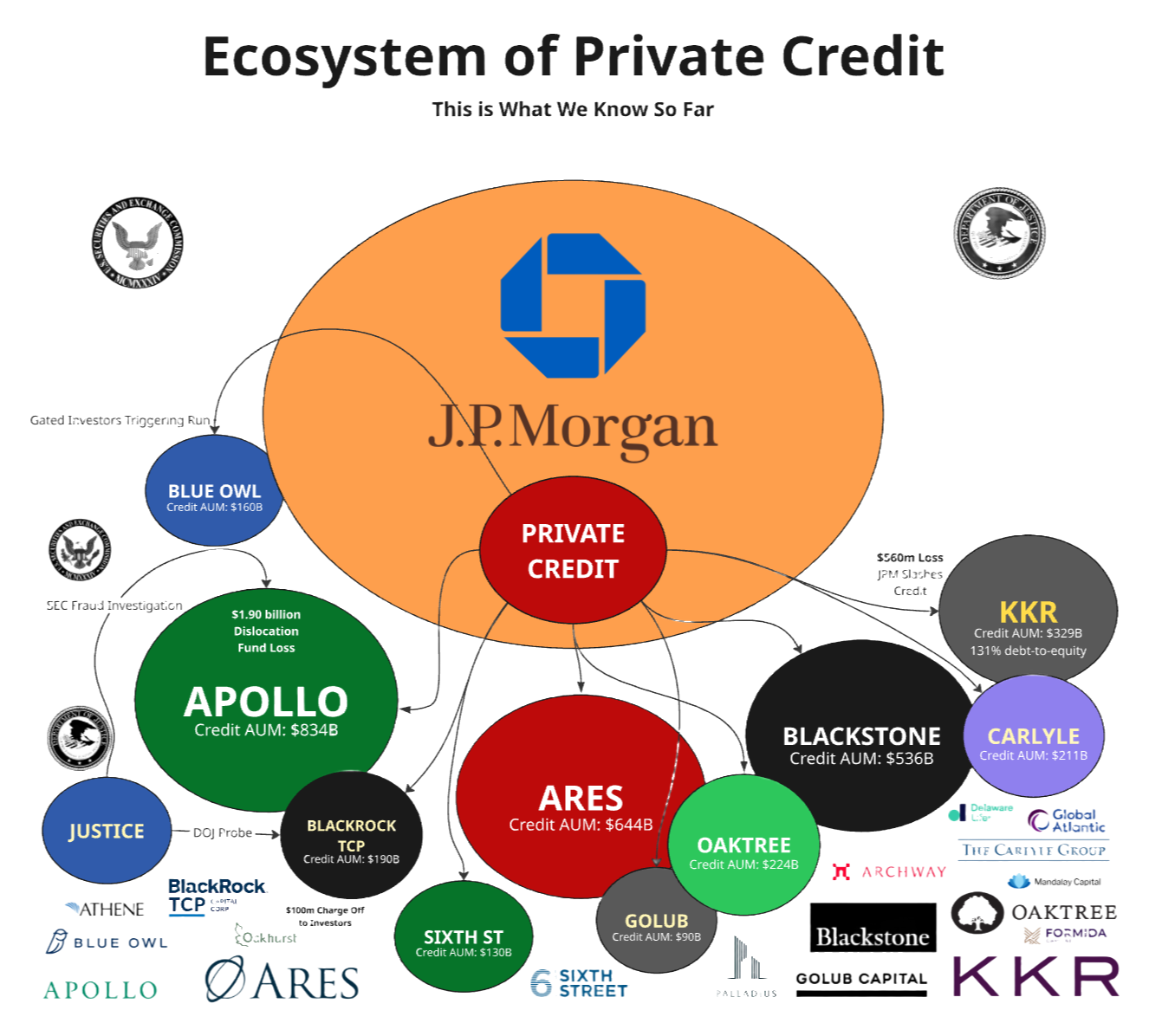

The pace quickened sharply in April and May 2026. On April 22, Blue Owl Capital found itself squarely in the spotlight. Co-founders Doug Ostrover and Marc Lipschultz had previously pledged massive amounts of company stock as collateral for personal loans—a structure that had provided insider liquidity when shares were riding high. The optics of using those pledged shares to purchase a hockey team, the Tampa Bay Lightning, did not help matters. As Blue Owl shares dropped sharply from peak levels, redemption pressure mounted in certain funds. Investors faced gating, the firm sold billions in loans to generate cash, and the founders abruptly replaced the pledged shares with other collateral. Bloomberg reported the unwind in real time. This was not mere housekeeping; it was a visible acknowledgment that the equity backing the personal financing was under pressure and that liquidity needs were forcing structural adjustments.

Just days later, on April 25, adjacent credit markets offered a cautionary parallel. Reports detailed how the U.S. sports-betting boom—fueled by mobile apps and widespread legalization—was pushing young Americans into bankruptcy at alarming rates. The Guardian and Business Insider highlighted the “out of control” gambling addiction, while research from the Federal Reserve Bank of New York and joint studies by UCLA, USC, and Harvard quantified rising delinquencies and consumer stress. While not a direct private-credit story, it illustrated a broader theme: when easy credit meets behavioral risk factors, repayment capacity erodes faster than static underwriting models predict. Private lenders with exposure to consumer-facing or discretionary businesses were already feeling the pinch.

Then on April 30, Starwood (SREIT), one of the nation’s most high-profile Real Estate Investment Trusts (REITs), blocked all withdrawals and cut distributions by 25% in an effort to stop investors from fleeing the plan. Starwood is not a small player. The fund owns 600 homes valued at $22 billion, highly leveraged with only $8 billion of equity, and $125 million in AUM. They made the move after getting elevated redemptions from investors.

May 2026 brought the story into sharper focus. On May 4, SEC Chairman Paul Atkins confirmed that the agency was investigating allegations of fraud at private credit firms while coordinating closely with the Treasury and the Federal Reserve. The same week, Apollo Global Management closed a $1.9 billion “dislocation” credit fund—capital explicitly raised to buy distressed assets when markets break. Sophisticated investors were not waiting for stress to materialize; they were positioning capital in advance which to regulators, looks a lot like fraud. That single closed fund spoke volumes about the probability distribution the smartest money saw coming.

The markdown wave hit in earnest between May 5 and May 7. Bloomberg and Reuters reported a cluster of developments that, taken together, painted a consistent picture of portfolio weakness:

- Sixth Street BDC cut its dividend after posting a quarterly loss.

- Oaktree marked down software loans with 26 percent AI exposure.

- Apollo reported losses on its private-credit portfolio of nearly $900 billion.

- Blue Owl BDCs repurchased $85 million of their own shares as loan values sank.

- BlackRock and Blackstone cut asset values in their private-credit vehicles.

These were not peripheral players. They were among the largest, most established names in the space. On May 7, additional institutional exposure surfaced to the tune of $1 billion: HSBC absorbed roughly a $400 million hit tied to leveraged private-credit structures it did not directly own on its balance sheet. JPMorgan and other banks faced hundreds of millions more in exposure after struggling to unload debt from leveraged buyouts. Jeffrey Gundlach warned publicly that private-credit investors could ultimately discover they would be the “bag holders.” The post-2008 narrative, that risk had been cleanly transferred out of the regulated banking system, began to look overly optimistic. Losses were finding pathways back through layered financing chains and structured vehicles.

May 12 delivered further evidence at scale. FS KKR Capital reported approximately $560 million in quarterly losses as nonaccrual loans surged to 8.1 percent. JPMorgan-led lenders responded by reducing the fund’s borrowing facility by $648 million and increased financing costs. KKR stepped in with a $300 million rescue package, including the purchase of shares from investors seeking exits. The stability narrative was fracturing at one of the industry’s flagship names precisely as inflation reaccelerated, and rate-cut expectations receded.

On May 16, federal prosecutors opened an investigation into valuation practices at BlackRock TCP Capital Corp following a massive markdown, a collapsing share price, and multiple investor class-action lawsuits. Unlike public loans, private credit is marked using internal models rather than market prices, potentially delaying the recognition of losses. If valuations are internal, they are simply valuing themselves. TCPC managed nearly $2 billion in middle-market loans, and there are suspicions that mismarking value was done to generate fees. Even John Zito of Apollo stated publicly, “...all the marks are wrong.” When regulators begin examining marks in earnest, investor trust erodes quickly; once trust erodes, the velocity of outflows accelerates.

May 23 shifted attention to the pension world. Public pensions collectively control roughly $6 trillion, with more than 36 million Americans relying on them for retirement security. CalPERS, the largest pension in America, faced an independent investigation commissioned by retiree advocates. When CalPERS—the bellwether for institutional behavior—moves aggressively into alternatives, smaller pension systems across the country tend to follow their lead. Despite CalPERS’ stonewalling and pushback, there were findings that raised governance questions relevant to every taxpayer and retiree whose future depends on those returns.

By early June, redemption pressure had become systemic. On June 3, investors attempted to withdraw more than $5 billion from Cliffwater’s flagship private-credit fund. Partners Group Limited withdrew from an $8.6 billion private-equity vehicle after requests surged. Moody’s turned negative on certain private-credit vehicles tied to rising corporate-loan defaults. Publicly traded shares of KKR, Blackstone, Ares, Blue Owl, and Carlyle sold off sharply. Redemption requests across U.S. non-traded private-credit vehicles reached as high as 41 percent in the first quarter of 2026. The question was no longer whether pressure existed; it was whether investors were beginning to treat private credit and private equity as a single interconnected system under strain.

June 4 added another fraud dimension: a former UBS-managed private-credit lender claimed a $145 million loss after relying on allegedly fraudulent financial statements. Assets that financials had shown at nearly $199 million proved to be worth less than $3,000. Trust across the sector that was already strained by valuation disputes, gates, and markdowns, was eroding further.

June 5 brought the most striking parallel to past crises. D.E. Shaw, one of the world’s largest hedge funds managing more than $90 billion, informed investors that it was locking up redemption timelines for its flagship fund for 4 years. The last time a major hedge fund announced such lock-ups was December 14, 2008, at the height of the financial system collapse, when Citadel locked up investor funds, suspending redemptions. Historically, long lock-ups were characteristic of private equity and private credit precisely because the assets were illiquid. Hedge funds were different.The move signaled that even sophisticated macro players were bracing for prolonged illiquidity. Is that because Private Credit has made its way inside of Hedge Funds as well?

Each of these episodes can be explained away individually. Collectively, they form a clear pattern: rising borrower stress from floating-rate coupons in a higher-for-longer environment; redemption demands outpacing available liquidity; forced asset sales or gates that crystallize losses; valuation disputes that invite regulatory scrutiny; and early signs of fraud or misrepresentation that further undermine confidence.

The Perfect Storm: Interest Rates, Expectations, and the Warsh Reality

At the center of this tension lies the interest-rate environment. Private-credit loans are overwhelmingly set at floating rates. A typical deal might price at SOFR + 5–7%. When short-term rates sat near zero in 2020–2021, the all-in coupon was easily serviceable for leveraged borrowers. As the Fed hiked aggressively through 2022–2023 to combat inflation, those coupons reset sharply higher—often landing in the 9–11 percent range or above. Borrowers who underwrote deals assuming rates would normalize quickly found themselves carrying debt-service burdens that consumed a far larger share of cash flow than projected.

Many fund managers and investors had positioned explicitly for rate cuts in 2024 and 2025. Models assumed a Fed pivot that would ease pressure, enable refinancing, and preserve equity-like upside. That expectation was reasonable based on historical precedent. It has not materialized as scripted. Inflation has proven stickier than anticipated, and economic data through mid-2026 continues to show resilience that, while positive on the surface, keeps the door open for tighter policy.

Kevin Warsh assumed the role of Federal Reserve Chair on May 22, 2026, succeeding Jerome Powell. For many market participants, Warsh was initially cast as a potential “savior”—a figure who might prioritize growth, deliver the rate relief the leveraged economy appeared to need, and perhaps even accommodate political pressure for easier policy. His background, however, tells a different story. Warsh served as a Fed governor from 2006 to 2011 and resigned in part over concerns about excessive easing and moral hazard. His public commentary has long emphasized financial stability, discipline, and the long-term costs of keeping rates artificially low. Against the backdrop of reaccelerating inflation signals and geopolitical tensions pushing oil prices higher, the prudent policy path, from his perspective, may well be to hold rates steady or even raise them if financial excesses threaten broader stability. This advisor believes the latter is inevitable.

That stance collides head-on with the hopes baked into much of the private-credit portfolio. Borrowers and lenders alike had counted on falling rates to provide breathing room. Instead, the higher-for-longer reality—combined with Warsh’s hawkish leanings—creates a classic perfect storm: elevated base rates that increase debt-service costs, slower economic repricing that delays relief, redemption pressure from investors running, not walking, to retrieve liquidity, and a policy backdrop that likely does not deliver the anticipated easing. Add in sector-specific vulnerabilities—AI software exposure, data-center leverage, and consumer businesses feeling the pinch from higher rates and behavioral stresses like sports betting—and the cumulative effect raises the probability of defaults, restructurings, and PIK toggles that merely defer rather than resolve underlying problems.

This dynamic is not abstract. It is playing out in real time across portfolios originated when rates were expected to fall. The result is a negative feedback loop: higher coupons help existing performing loans in theory, but they simultaneously strain marginal borrowers, increase nonaccruals, and force managers to sell higher-quality assets to meet redemptions—leaving remaining portfolios with weaker average credit quality.

Mission Creep: How Private Credit Quietly Entered Everyday Retirement Accounts and 401Ks

What makes this recalibration particularly relevant and disturbing to ordinary investors is the quiet, opaque migration of private credit into retirement savings. Collective Investment Trusts (CITs) have grown dramatically over the past decade and a half. According to Department of Labor data reported by Bloomberg on May 4, 2026, CITs now hold roughly 40 percent of 401(k) assets—up from just 12 percent in 2010. The total CIT market is estimated at $6–7 trillion. These vehicles operate under a fragmented system of bank and labor oversight rather than full SEC registration. They are not required to publish daily holdings or net asset values, as mutual funds are. Reporting is inconsistent, and visibility for plan participants remains limited.

Retirement money has been moving out of Transparent Public Structures, like Mutual Funds, and into Opaque Pooled Private Assets. CITs have become the primary gateway for these private assets—real estate investment trusts, private equity, and private credit—slipping into defined-contribution plans. Over $54 billion shifted from mutual funds into CITs in 2025 alone. Large plans now allocate nearly half of their assets through these structures, and proposed regulatory expansions could unlock another $1.5 trillion in 403(b) plans. Target-date funds, the default investment option for millions of participants who never actively choose their allocations, increasingly include slices of alternatives through CIT wrappers. Most participants have no idea that their “balanced” or “growth” fund now contains illiquid loans to middle-market companies, often with floating-rate exposure and redemption restrictions.

Public pensions offer a parallel window into the governance challenges. CalPERS, managing more than $630 billion for 2.4 million beneficiaries, has significant exposure to private debt. An independent investigation released in May 2026, commissioned by retiree advocates and led by forensic experts, highlighted chronic underperformance, billions locked in aging private-equity and private-credit partnerships, hidden fees, conflicts of interest, and a lack of transparency. The mission creep is now complete: what began as a tool for sophisticated institutional investors has, through CITs and target-date glide paths, become an indirect holding for teachers, firefighters, nurses, police officers, and office workers who simply checked the box on their employer’s retirement-plan enrollment form. So, when the nation’s largest public pension system increases allocations to these highly illiquid asset classes, everyone should be asking, “Why?”

This opacity carries real consequences. When redemptions are gated at the fund manager level, the impact does not appear as a visible share price drop on a 401(k) statement. Instead, it shows up as slower capital return, forced sales elsewhere in the portfolio, or quietly lower performance in future quarters. Participants may not recognize the problem until quarterly statements reflect restricted access or reduced balances. The risk is not that every private-credit loan defaults. The risk is that the mismatch between promised liquidity and actual asset liquidity becomes apparent precisely when confidence in valuations begins to wane. At that point, the velocity of outflows from retail vehicles can accelerate the pressure on the entire ecosystem.

How Stress Propagates: From Private Credit to Broader Markets and Banking

The transmission mechanism from private credit stress to the wider economy and banking sector is not theoretical. It follows the physics of capital flow. Banks, after 2008, offloaded much of their direct lending risk through originate-to-distribute models and participation in syndicated leveraged loans. Insurance companies, pensions, endowments, and now retail investors via CITs became the new reservoirs holding the paper. When inflows were robust and redemptions modest, the system absorbed shocks. Now, with redemption requests climbing to 41 percent in some vehicles in the first quarter of 2026, managers are selling what they can—often the higher-quality loans—to meet withdrawals. This leaves portfolios with weaker average credit metrics, which in turn prompts further markdowns and erodes confidence.

Banks that provided warehouse lines, revolvers, or participated in leveraged-buyout financing now face margin calls, reduced facilities, or outright losses when collateral values decline. The May 2026 reports of HSBC absorbing a $400 million hit from supposedly off-balance-sheet structures and JPMorgan struggling to unload leveraged debt illustrate how quickly layered financing can bring risk back onto regulated balance sheets. Corporate borrowers facing higher coupons delay capital expenditures, renegotiate terms, or restructure. Suppliers, employees, and local economies feel the secondary effects. Public markets, already attuned to any hint of credit deterioration, price in the risk through wider spreads, equity volatility, and sell-offs in the shares of the private-credit managers themselves.

The analogy to the 19th-century railroad bubble is apt, not alarmist. Massive capital flowed into transformative infrastructure that promised endless growth. Overbuilding, leverage, and optimistic assumptions about perpetual expansion led to a reckoning when cash flows failed to match projections. Today’s AI-driven boom carries echoes: enormous commitments to data centers and software, floating-rate structures predicated on continued low or falling rates, and a widespread belief that technological transformation would outrun financial constraints. Bank of America strategist Michael Hartnett captured the sentiment when he described the current environment as “the biggest bubble since the railroads.” The parallel lies not in the specific asset class but in the psychology of flow—capital rushing in on narrative, then potentially rushing out when reality intervenes.

`

This setup bears the hallmarks of a hybrid dot-com and 2008 crisis. The dot-com element is the speculative overvaluation and leverage tied to transformative technology (AI, in this case), in which growth expectations outrun sustainable cash flows. The 2008 element is the hidden leverage, opacity, and contagion risk that travels through off-balance-sheet structures and back into the banking system when liquidity evaporates. Private credit sits at the intersection: it finances the tech-leverage story while operating in a largely unregulated, illiquid space that was supposed to insulate banks. Instead, it is creating pathways for stress to migrate back.

Understanding Flow and Velocity: The Real Market Dynamic

Markets are less about directional price moves and more about the volume and velocity of capital. Picture a riverbed. In normal times, steady inflows keep the water level manageable. When inflows slow and outflows accelerate simultaneously, the channel narrows, velocity increases, and what was once a gentle current becomes a torrent capable of eroding banks and overflowing into adjacent areas.

In private credit, the volume of committed capital is enormous. The velocity is now shifting. Redemption requests that once represented 5–10 percent of fund assets are hitting 17–41 percent in some vehicles. Managers respond by selling assets, gating, or injecting rescue capital. Each action alters the flow for everyone else in the system. Banks feel the pressure on warehouse lines. Public markets price in risk through manager stock sell-offs. Retirement savers experience it indirectly through CIT performance. The danger lies in how quickly velocity can compound: a modest increase in outflows begets markdowns, which beget more outflows, which force further sales at distressed levels.

This is why the railroad-bubble comparison resonates. It was not a single event but a rapid reversal of capital flow once confidence cracked. The same dynamic applies today. Private credit is not inherently flawed; it serves a legitimate economic function in financing companies that banks have stepped away from. But when scale, leverage, and liquidity assumptions meet a higher-rate environment and shifting investor sentiment, the velocity of capital seeking safety becomes the dominant variable.

Practical Advisory Guidance: What You Should Do Now

None of this guarantees a systemic meltdown. Private credit still finances real businesses. Many loans remain performing. Experienced managers have tools—covenants, collateral, restructuring expertise—to mitigate losses. Regulatory scrutiny, while uncomfortable in the short term, can improve standards over the long run. Yet the prudent investor must acknowledge the setup and act accordingly.

First, know your exposure. Review every 401(k), IRA, pension statement, and advisory account. Ask explicitly whether CITs, target-date funds, or any alternative sleeves contain private credit, private equity, REITs, or other illiquid assets. Request the underlying holdings or strategy documents. If your advisor or plan administrator cannot provide clear, timely answers, that itself is valuable information. Opacity is a risk factor. Brace for impact. In a liquidity crisis, these funds have the potential to fail.

Second, stress-test your liquidity needs. If you anticipate needing access to capital within the next 12–36 months—for retirement distributions, college tuition, medical expenses, or any other reason—ensure your overall portfolio maintains sufficient truly liquid reserves outside of private-credit vehicles. Typically, illiquid assets should not exceed 5-10% of the overall portfolio value, even for accredited investors. Positions that once seemed quarterly-liquid may return capital more slowly than expected under current conditions, or stop altogether.

Third, examine cash-flow realities. For any direct or indirect private-credit holdings, understand the weighted-average coupon, reset frequency, borrower leverage metrics, and industry concentrations. Rising rates have helped coupons on performing loans, but they have simultaneously increased stress on marginal borrowers. Track nonaccrual rates, PIK usage, and any dividend cuts at BDCs as early warning signals.

Fourth, monitor the flow signals. Elevated redemption requests, sudden collateral swaps by insiders, increased rescue capital injections, valuation disputes under SEC or DOJ scrutiny, and Moody’s negative outlooks are not routine housekeeping. Treat them as data points indicating shifting velocity. Diversify thoughtfully. Private credit may belong in an accredited investor’s portfolio as part of a broader allocation, but size it appropriately relative to liquid assets, age, and risk tolerance. Investors approaching or in retirement should be wary of Private Credit or Private Equity in their portfolios. Consider the velocity risk explicitly rather than assuming historical liquidity patterns will hold.

Fifth, engage in governance. If you are a plan sponsor, fiduciary, or participant representative overseeing CITs or pension assets, demand better transparency and independent valuation reviews. The Department of Labor and the SEC are already increasing attention; beneficiaries should do the same. For individual investors, consider working with advisors who specialize in stress-testing illiquid allocations rather than simply accepting the standard allocation models.

Finally, maintain perspective. Markets have rewarded risk-taking for years. They have also reminded us repeatedly that the cost of complacency arrives not as a single thunderclap but as a rising water level that eventually overtakes the levees. The prudent move is not to bet against the house but to understand the table, count the cards you can see, and keep enough chips in reserve—both financial and psychological—to weather whatever the next roll brings.

Preparation Over Prediction

The dice are still rolling. Private credit is not the villain in this story; it is simply the latest iteration in a long financial history where innovation, yield hunger, and optimistic liquidity assumptions meet the hard edge of economic reality, hubris, and greed. The events from late 2025 through June 2026—the markdowns at Blue Owl, Apollo, BlackRock, and others; the gating at Cliffwater and Partners Group; the regulatory inquiries from the SEC and DOJ; the pension-level scrutiny at CalPERS; the extension of lock-ups at D.E. Shaw; and the policy backdrop under Chairman Warsh—provide a clearer map of the terrain ahead.

People should be concerned. The hybrid nature of the risks—dot-com-style technological exuberance layered atop 2008-style credit opacity and banking transmission—warrants serious attention to investments and potential spillovers in the banking sector. It means informed caution, transparent questioning of advisors, getting second opinions, repositioning or diversifying into non-correlated assets, and deliberate portfolio construction that respects the physics of flow and velocity.

Markets reward preparation more reliably than prediction. In that spirit, the cautious, informed investor remains best positioned to navigate the currents—whatever their direction or speed. What goes up can indeed go higher. But when the flow reverses, velocity dictates the terms, and it can happen in a flash. Prepare accordingly.

Richard Bavetz, ChFC®, CLU®, FRC℠ is a Chartered Financial Consultant® (ChFC®), a Chartered Life Underwriter®, a Federal Retirement Consultant℠ and an Investment Advisor with over 28 years of experience. As a Fiduciary, he works with High-Net-Worth investors, Foundations and Endowments, offering dynamic & innovative investment portfolios in a relationship-centered advisory role. This overview is for educational purposes only. The information herein is deemed reliable but not guaranteed. Always consult a licensed Investment Advisor, Fiduciary, insurance professional, tax advisor, and financial planner for a personalized risk assessment and suitability analysis.

Complete Source Articles List:

April 2026

According to TREPP data:

Delinquencies jumped to 7.55% in March

If you include “performing matured” loans, it’s over 9%

Office delinquencies are near 12%

Multifamily is now cracking

Lodging just spiked past 7%

TREPP (CMBS delinquency data)

MSCI (distressed sales volume)

The Wall Street Journal (office market losses)

Green Street (valuation declines)

RentCafe (conversion data)

The Wall Street Journal — CDS index development on private credit

JPMorgan Chase — Lead bank involvement

S&P Global — Index construction

Market structure comparison to 2008 CDS expansion and **American International Group exposure

S&P Global: “The ecosystem exhibits an inherent fragility that could be tested under severe stress.”

PNC Financial Services — Q1 2026 earnings release and disclosures (April 2026)

Truist Financial — Q1 2026 earnings presentation (April 2026)

U.S. Bancorp — Q1 2026 earnings materials (April 2026)

Regions Financial — Q1 2026 investor presentation (April 2026)

Fifth Third Bancorp — earnings disclosures (April 2026)

KeyCorp — earnings disclosures (April 2026)

Huntington Bancshares — earnings disclosures (April 2026)

Aggregated regional bank NDFI exposure reporting (Reuters earnings coverage, April 2026)

Bloomberg — “Blue Owl Founders Remove Stock as Collateral After Share Slump” April 22, 2026

Bloomberg — “Blue Owl Loan Sale Raises $1.4 Billion for Investor Payouts” February 18, 2026

Additional context:

Public filings by Blue Owl Capital

Market data on OWL share price decline

National Credit Union Administration — 2025 & 2026 Supervisory Priorities

National Credit Union Administration — Q4 2025 Credit Union System Data

Navy Federal Credit Union — 2025 Annual Report

PenFed Credit Union — 2024 Annual Report

State Employees’ Credit Union — 2025 Financials

“US gambling addiction is ‘out of control’ as betting markets boom, policy expert warns” — The Guardian

“Online sports betting boom is pushing young Americans into bankruptcy” — Business Insider

Federal Reserve Bank of New York — research on credit outcomes following sports betting legalization

UCLA / University of Southern California / Harvard — joint research on bankruptcy and delinquency impacts from mobile betting expansion

The Wall Street Journal (April 28, 2026) — OpenAI missed internal projections for revenue and user growth; internal concerns over funding future compute contracts

CNBC (April 28, 2026) — AI infrastructure stocks fall following report of OpenAI missing growth expectations

Market data (April 28, 2026):

Oracle decline tied to ~$300B OpenAI compute partnership

Nvidia, AMD, Broadcom down ~3–5%

CoreWeave down ~7%

SoftBank down ~10%

Financial Times: “Starwood real estate fund halts redemptions as bet on lower interest rates bites”

Statement from Barry Sternlicht (via FT reporting)

Fund data and portfolio details from Starwood disclosures

Market context on redemption limits across private real estate and credit funds

May 2026

Bloomberg reports May 4, 2026:

Trillions of Retirement Dollars Flow into Opaque Trusts

~40% of 401(k) assets are now in CITs (Department of Labor data)

Total CIT assets estimated between $6 trillion and $7 trillion

Over $54.3 billion shifted from mutual funds into CITs in 2025 alone (Morningstar)

Large plans now hold nearly half of assets in CITs

A proposed expansion could open another $1.5 trillion (403(b) plans) to these structures

Bloomberg — SEC investigation comments by Paul Atkins (May 4, 2026, Milken

Reuters — Apollo closes Accord VII fund with $1.9B in commitments (May 4, 2026)

Bloomberg — Apollo Accord VII fund close and dislocation strategy

Financial Times — “Banks seek to offload risk to avoid ‘choking’ on data centre debt”

The Wall Street Journal — reporting on hyperscaler AI spending projections, financing constraints, and debt-market dependence tied to AI infrastructure expansion

Zero Hedge — “Banks Are Choking”: The AI Debt Bubble Has Started To Burst

Commentary from Man Group credit-risk executives regarding concentration and bank-capacity stress tied to AI infrastructure financing

Financial Times — “HSBC hit by losses linked to Apollo-backed financing structure” (May 2026)

Bloomberg — “JPMorgan and banks stuck with debt tied to leveraged buyout financing” (May 2026)

Bloomberg Television interview / Jeffrey Gundlach comments warning private credit investors could become “bagholders” (May 2026)

ZeroHedge - "Gundlach Warns "Bagholders" Will "Lose Money" In Private Credit As BDCs Slash Asset Values, JPM Faces $500MM Loss In Biggest "Hung" Deal This Year"

Financial Times — Bank of England comments regarding layered leverage and private credit exposure structures (May 2026)

Bloomberg — “Sixth Street BDC Cuts Its Dividend After Posting Quarterly Loss” — May 5, 2026

Bloomberg — “Oaktree BDC Marks Down Software Loans, Flags 26% AI Exposure” — May 5, 2026

Bloomberg — “Apollo Private Credit Fund Reports Loss on Portfolio Weakness” — May 6, 2026

Bloomberg — “Blue Owl BDCs Buy Back $85 Million of Shares as Loan Values Sink” — May 6, 2026

Bloomberg — “BlackRock Private Credit Fund Cuts Asset Value on Markdowns” — Updated May 7, 2026

Reuters — “Blackstone, BlackRock cut value of their private credit funds” — May 7, 2026

CNBC — “JPMorgan Chase-led bank group reins in credit line to troubled KKR private credit fund as losses mount” — May 11, 2026

Reuters — “KKR to plough $300 million into private credit fund as losses mount” — May 11, 2026

Barron’s — “JPMorgan Restricts Private-Credit Lending. Why Blue Owl, KKR Stocks Are Falling.” — May 2026

Barron’s — “KKR Private-Credit Fund Loans Sour as Losses Mount” — May 2026

Wall Street Journal — “KKR Private-Credit Fund Takes $560 Million Loss” — May 2026

Bloomberg — “US Prosecutors Probe BlackRock TCP Capital Valuation Practices” — May 15, 2026

Bloomberg — “BlackRock TCP Capital Slides After Warning on Asset Values” — January 2026

Public investor class action filings relating to BlackRock TCP Capital Corp. valuation disclosures and investor claims — 2026

Bloomberg — “US 30-Year Yield Hits Highest Since 2007 on Inflation Angst” -May 19, 2026

Financial Times — “Investors warn of ‘correction’ risk as high-flying stocks defy bond gloom” — May 18, 2026

Bank of America Global Fund Manager Survey — May 2026

Reuters - “JPMorgan looks to offload exposure to $4 billion in private equity-linked loans” - May 21, 2026

CNBC Pro — “Private Credit Defaults Hit Record High as Interest Rates Soar”— May 21, 2026

Fitch Ratings — “Fitch Ratings’ U.S. Private Credit Default Rate Hits High of 6.0% in April 2026” — May 18, 2026

Financial Times - “Private equity's new escape hatch keeps unsold companies in limbo” - May 21, 2026

NBC News — “Nation’s largest public pension fund plagued by secrecy and underperformance, probe finds” (May 2026)

California Public Employees’ Retirement System (CalPERS) — Recent performance and asset reports (2025–2026)

Edward Siedle (former SEC attorney and forensic pension investigator) — Independent CalPERS investigation commissioned by retiree advocacy organizations (2026)

Andrew J. Bowden, SEC Director of Compliance Inspections and Examinations — Private Equity Speech Regarding Fees and Expenses (May 6, 2014)

The Real Deal — “JPMorgan pulls plug on $1.4B real estate fund after years of losses” — May 26, 2026

Bisnow reporting referenced within The Real Deal article regarding liquidation plans

IPE Real Assets reporting regarding Ohio Bureau of Workers’ Compensation documents tied to the fund

Forbes — “Rising Private Credit Defaults Are Testing Banks And Insurers” — May 24, 2026

Forbes — “Private credit is the lowest quality asset class across our leveraged finance universe,” said **Neha Khoda**, head of U.S. credit strategy at BofA.

Fitch Ratings — U.S. Private Credit Default Data referenced in Forbes article (May 2026)

Moody’s — Distressed Exchange and Restructuring Analysis referenced in Forbes article

Proskauer Private Credit Default Index Q1 2026 referenced in Forbes article

June 2026

Financial Times — “Partners Group limits withdrawals from private equity fund after redemption requests surge” — June 3, 2026

Bloomberg — Partners Group reports elevated redemption requests and limits withdrawals from flagship private-equity vehicle — June 3, 2026

Financial Times — “Cliffwater private credit fund limits withdrawals after redemption requests reach 17%” — June 2, 2026

Moody’s Ratings — Negative outlook actions tied to Blackstone and Golub private-credit vehicles due to rising corporate-loan defaults — June 2026

Bloomberg — Private-market stocks sell off following Partners Group withdrawal restrictions — June 3, 2026

Reuters - US asset managers fall as investors brace for updates on private credit fund withdrawals- June 3, 2026

Financial Times - “Former UBS private credit fund says law firm helped defraud it of $145mn” -June 3, 2026

Reuters – U.S. prosecutors examining private market valuation practices – June 3, 2026

Financial Times — “D.E. Shaw Extends Investor Exit Time to Four Years for Flagship Fund” — June 3, 2026

Financial Times — Coverage of hedge fund redemption restrictions during the 2008 financial crisis

Financial Times — “Blackstone explores $2bn-plus private equity CFO deal” - June 8, 2026

Bloomberg — Columbia Researchers Challenge Private Credit Ratings -June 8, 2026

Bloomberg — U.S. Life Insurers Hold $807 Billion of Illiquid Credit Assets -June 8 2026

Seeking Alpha “A credit loss cycle has begun, own quality debt - PIMCO analysts” - June 10, 2026

CNBC “Oracle shares tumble 11% on increased capital raise, cash concerns” -June 11, 2016

Bloomberg “America’s Car-Mart Seeking Financing, Discussing Potential Chapter 11 Filing” -June 11, 2026

Source Links

TREPP CMBS Delinquency Data (7.55% in March 2026, office near 12%, lodging spike past 7%, multifamily cracking):

- Trepp Official Report: https://www.trepp.com/trepptalk/cmbs-delinquency-rate-jumps-in-march-2026 (March 31, 2026)

- Multifamily Dive coverage: https://www.multifamilydive.com/news/multifamily-cmbs-delinquency-apartment-loan-default/816842/ (April 7, 2026)

Blue Owl Founders Remove Stock as Collateral (April 2026, related to share slump):

- Bloomberg: https://www.bloomberg.com/news/articles/2026-04-17/blue-owl-co-ceos-personal-loans-no-longer-backed-by-firm-shares (April 17, 2026)

- WSJ: https://www.wsj.com/finance/investing/blue-owl-founders-revise-terms-of-personal-loans-that-raised-scrutiny-9f6bee3f (April 17, 2026)

- https://www.bloomberg.com/news/articles/2026-02-18/blue-owl-loan-sale-raises-1-4-billion-for-investor-payouts (February companion piece).

“US gambling addiction is ‘out of control’” — The Guardian:

- https://www.theguardian.com/us-news/2026/apr/24/gambling-addiction-out-of-control-betting-markets

National Credit Union Administration — 2025 & 2026 Supervisory Priorities:

- https://ncua.gov/regulation-supervision/letters-credit-unions-other-guidance/ncuas-2025-supervisory-priorities

- https://ncua.gov/regulation-supervision/letters-credit-unions-other-guidance/ncuas-2026-supervisory-priorities

OpenAI Missed Internal Projections (WSJ, April 28, 2026) and AI stocks fallout:

- WSJ: https://www.wsj.com/tech/ai/openai-misses-key-revenue-user-targets-in-high-stakes-sprint-toward-ipo-94a95273 (April 28, 2026)

- CNBC on stock impact: https://www.cnbc.com/2026/04/28/openai-reportedly-missed-revenue-targets-shares-of-oracle-and-these-chip-stocks-are-falling.html (April 28, 2026)

Starwood Real Estate Fund Halts Redemptions (FT):

- FT: https://www.ft.com/content/19cf1211-f2b7-48bc-ae8b-8c36c8d3da40 (April 30, 2026)

Trillions of Retirement Dollars into Opaque Trusts / CITs (Bloomberg, ~May 4, 2026):

- Bloomberg: https://www.bloomberg.com/news/features/2026-05-03/trillions-in-us-retirement-dollars-flow-into-opaque-trusts-that-rival-etfs (May 3, 2026)

Sixth Street BDC Cuts Dividend After Loss (Bloomberg, May 5, 2026):

- Bloomberg: https://www.bloomberg.com/news/articles/2026-05-05/sixth-street-bdc-cuts-its-dividend-after-posting-quarterly-loss (May 5, 2026)

JPMorgan Pulls Plug on $1.4B Real Estate Fund (May 26, 2026):

- The Real Deal: https://therealdeal.com/national/2026/05/26/jpmorgan-pulls-plug-on-1-4b-real-estate-fund-after-losses/ (May 26, 2026)

Financial Times — “Banks seek to offload risk to avoid ‘choking’ on data centre debt”:

- https://www.ft.com/content/08aba5e4-5834-4e79-a48d-989a2c5bad0f

Financial Times — “HSBC hit by losses linked to Apollo-backed financing” / other private credit pieces:

BlackRock TCP Capital Valuation Probe (Bloomberg, May 15, 2026):

- Bloomberg: https://www.bloomberg.com/news/articles/2026-05-15/blackrock-private-credit-fund-s-valuations-being-probed-by-doj (May 15, 2026)

KKR Private-Credit Fund Losses (~$560M, May 2026):

- WSJ: https://www.wsj.com/finance/investing/kkr-private-credit-fund-takes-560-million-loss-f6bfb576 (May 11, 2026)

- Reuters: https://www.reuters.com/legal/transactional/kkr-plough-300-million-into-private-credit-fund-losses-mount-2026-05-11/ (May 11, 2026)

The Real Deal — “JPMorgan pulls plug on $1.4B real estate fund” (May 26, 2026):

- https://therealdeal.com/national/2026/05/26/jpmorgan-pulls-plug-on-1-4b-real-estate-fund-after-losses/

Partners Group Limits Withdrawals (FT/Bloomberg, June 3, 2026):

- FT: https://www.ft.com/content/c41346b0-05be-4d57-9d14-e90a018f5e25 (June 3, 2026)

- Bloomberg: https://www.bloomberg.com/news/articles/2026-06-03/partners-group-gates-evergreen-fund-as-redemption-requests-rise (June 3, 2026)

- Reuters: https://www.reuters.com/world/partners-group-caps-withdrawals-86-billion-fund-shares-plunge-2026-06-03/ (June 3, 2026)

America’s Car-Mart Seeking Financing / Potential Chapter 11 (Bloomberg, June 11, 2026):

- Bloomberg: https://www.bloomberg.com/news/articles/2026-06-10/subprime-auto-dealer-america-s-car-mart-seeks-rescue-financing (June 10, 2026)

Quote Source:

Reuters (December 9, 2025) — “US private credit defaults to ease in 2026, but fragility to persist, says BofA”

Direct Quote:

“Private credit is the lowest quality asset class across our leveraged finance universe,” said **Neha Khoda**, head of U.S. credit strategy at BofA.

Links:

- Reuters (Dec 09, 2025): Bank of America’s credit strategy team using this description in the context of rising defaults.

https://www.reuters.com/business/finance/us-private-credit-defaults-ease-2026-fragility-persist-says-bofa-2025-12-09/

- Forbes (May 24, 2026): Bank of America’s credit strategy team using this description in the context of rising defaults.

https://www.forbes.com/sites/mayrarodriguezvalladares/2026/05/24/rising-private-credit-defaults-are-testing-banks-and-insurers/

- Multiple secondary sources (LinkedIn summaries, Insurance Business Magazine, etc.) repeat the quote from the original BofA commentary via Reuters.

Context on “Lowest Quality” Quote:

This comment from BofA’s credit strategy team (led by Neha Khoda) has been frequently cited in 2026 coverage amid discussions of private credit defaults, markdowns, and bank/insurer exposure. It aligns with the broader April–June 2026 perspective of events (e.g., BDC markdowns, fund redemptions, and stress in the asset class).

Quote Source:

Main Bloomberg TV Appearance:

Date: May 7, 2026

Show: *Bloomberg The Close* (live from DoubleLine’s L.A. offices)

Direct Quote:

Jeffrey Gundlach Bloomberg Television Interview (May 2026) – “Bagholders” Warning on Private Credit**

Links:

- Bloomberg Video: https://www.bloomberg.com/news/videos/2026-05-07/gundlach-warns-about-the-risks-facing-private-credit-video

(Gundlach discusses private credit risks, compares the market to 2007 conditions, and highlights potential domino effects.)

- Full Segment (DoubleLine upload): https://www.youtube.com/watch?v=1yCyGFZMQng

(“Jeffrey Gundlach on Private Credit's Wild West and a U.S. Debt Tail Risk” – opens with a stark warning on private credit, redemption pressures, and “laundered volatility.”)

- Companion Bloomberg Article (May 6, 2026): https://www.bloomberg.com/news/articles/2026-05-06/gundlach-warns-investors-will-lose-money-on-private-credit-funds

(Details Gundlach’s comments on investors potentially becoming “bagholders,” criticism of semi-liquid funds, financial intermediaries, and high fees.)

- ZeroHedge Summary (May 7, 2026): https://www.zerohedge.com/markets/gundlach-warns-bagholders-will-lose-money-private-credit-bdcs-slash-asset-values-jpm-faces (explicitly uses “bagholders” in the headline and quotes).

- DoubleLine Official Page: https://doubleline.com/markets-insights/jeffrey-gundlach-on-private-credits-wild-west-and-a-u-s-debt-tail-risk-bloomberg-tv/ (May 7, 2026)

Context on “Bagholders” Quote:

Gundlach warned that retail and other investors in private credit (especially semi-liquid/interval funds) are starting to realize they might be the “bagholders” as redemption requests rise and underlying issues (opacity, markdowns, gating) become clear. He drew parallels to past bubbles (dot-com, pre-2008 mortgages) and criticized the marketing of illiquidity as a “feature.”

Quote Source:

CNBC (March 16, 2026) https://www.cnbc.com/2026/03/16/apollo-john-zito-private-equity-software-valuations.html

(CNBC independently confirmed the audio and quotes.)

Direct Quote:

“I literally think all the marks are wrong. Is that what you’re asking me? I think private-equity marks are wrong.” Made in remarks to UBS clients in February 2026

Links:

- Wall Street Journal (Original/Best Reporting – March 15, 2026) https://www.wsj.com/finance/investing/top-apollo-executive-sounds-off-on-arrogance-in-private-markets-4f09b5cb

(Details the full comments on “arrogance” in private markets, software valuations, and potential loan recoveries of 20–40 cents on the dollar.)

- CNBC (March 16, 2026) https://www.cnbc.com/2026/03/16/apollo-john-zito-private-equity-software-valuations.html

(CNBC independently confirmed the audio and quotes.)

- Yahoo Finance / Investing.com Summary (March 16–17, 2026) https://finance.yahoo.com/news/apollo-exec-says-private-equity-185241593.htmlApollo clarified that Zito was specifically referring to software company valuations in private equity portfolios (where Apollo has low exposure), amid sharp declines in public software stocks due to AI disruption.

Context on “All the Marks are Wrong” Quote:

This statement gained significant traction in March–May 2026 private credit and valuation discussions, especially as BDC markdowns, redemption pressures, and probes into marking practices intensified. It is frequently cited alongside broader 2026 concerns about opaque private market valuations.

Many Bloomberg, Financial Times, and WSJ articles are paywalled or region-restricted. Email rick@yourcaringadvisor.com for a copy of any source article.

April 2026 Bank Q1 Earnings Filings & Investor Relations Materials (April 2026 releases):

PNC Financial Services — Q1 2026 Earnings:

- Earnings Release: https://investor.pnc.com/news-events/financial-press-releases/detail/684/pnc-reports-first-quarter-2026-net-income-of-1-8-billion-4-13-diluted-eps-or-4-32-as-adjusted (April 15, 2026)

-EarningsPresentation: https://d1io3yog0oux5.cloudfront.net/_dffbb0389228153a0fb81378bd61001a/pnc/db/2321/24010/pdf/1Q26+Earnings+Slides.vf.pdf

- Investor Relations Hub: https://investor.pnc.com/

- SEC Filings: https://investor.pnc.com/sec-filings/all-sec-filings

Truist Financial — Q1 2026 Earnings:

- Earnings Release & Presentation: https://ir.truist.com/2026-04-17-Truist-reports-first-quarter-2026-results (April 17, 2026)

- Events & Presentations (with 1Q26 materials): https://ir.truist.com/events-and-presentation

- Earnings Page: https://ir.truist.com/earnings

U.S. Bancorp — Q1 2026 Earnings:

- Earnings Release: https://ir.usbank.com/news-events/news/news-details/2026/U-S--Bancorp-Reports-First-Quarter-2026-Results/default.aspx (April 16, 2026)

- Investor Relations / Quarterly Results: https://ir.usbank.com/

- SEC Filings: https://ir.usbank.com/financials/sec-filings/default.aspx

Regions Financial — Q1 2026 Investor Presentation & Earnings:

- Earnings Release: https://ir.regions.com/news-events/press-releases/news-details/2026/Regions-Reports-earnings-of-539-million-and-EPS-of-0-62-in-1Q-2026/default.aspx (April 17, 2026)

- Quarterly Investor Info: https://ir.regions.com/financial-information/quarterly-investor-info/default.aspx

- IR Hub: https://ir.regions.com/

Fifth Third Bancorp — Q1 2026 Earnings Disclosures:

- Earnings Release: https://ir.53.com/news/news-details/2026/Fifth-Third-Bancorp-Reports-First-Quarter-2026-Earnings/default.aspx (April 17, 2026)

- Earnings Presentation: https://s23.q4cdn.com/252949160/files/doc_financials/2026/q1/Fifth-Third-Bancorp-Presentation-Q126-Final.pdf

- Quarterly Reports: https://ir.53.com/financial-information/quarterly-and-annual-reports/default.aspx

KeyCorp — Q1 2026 Earnings:

- Earnings Release: https://investor.key.com/press-releases/news-details/2026/KEYCORP-REPORTS-FIRST-QUARTER-2026-NET-INCOME-OF-486-MILLION-OR-0-44-PER-DILUTED-COMMON-SHARE-INCREASING-33-YEAR-OVER-YEAR/default.aspx (April 16, 2026)

- Quarterly Earnings Results: https://investor.key.com/financials/quarterly-earnings-results/default.aspx

Huntington Bancshares — Q1 2026 Earnings:

- Earnings Release: https://ir.huntington.com/news-presentations/press-releases/detail/991/huntington-bancshares-incorporated-reports-2026-first-quarter-earnings (April 23, 2026)

- Financial Results: https://ir.huntington.com/financial-information/financial-results

Blue Owl Capital (OWL) Public Filings:

- IR / SEC Filings: https://ir.blueowl.com/Investors/financials/sec-filings/default.aspx

- Q1 2026 Results: https://www.blueowl.com/news/blue-owl-capital-inc-first-quarter-2026-results (April 30, 2026)

- Related BDC filings (e.g., OBDC): https://www.blueowlcapitalcorporation.com/investors/sec-filings

National Credit Union Administration (NCUA):

- 2025 Supervisory Priorities: https://ncua.gov/regulation-supervision/letters-credit-unions-other-guidance/ncuas-2025-supervisory-priorities (January 2025)

- Q4 2025 Credit Union System Data: https://ncua.gov/newsroom/press-release/2026/ncua-releases-fourth-quarter-2025-credit-union-system-performance-data (March 6, 2026)

- Letters & Guidance: https://ncua.gov/regulation-supervision/letters-credit-unions-other-guidance

Credit Union Annual Reports:

- Navy Federal Credit Union 2025 Annual Report: https://www.navyfederal.org/content/dam/nfculibs/pdfs/financial-reports/2025-annual-report.pdf (May 2026)

- Older Navy Federal reports: https://www.navyfederal.org/about/operations.html

CalPERS Performance & Asset Reports (2025–2026):

- Preliminary FY 2024-25 Return: https://www.calpers.ca.gov/newsroom/calpers-news/2025/calpers-announces-preliminary-116-return-for-2024-25-fiscal-year (July 2025)

- Investment & Financial Reports: https://www.calpers.ca.gov/investments/about-investment-office/investment-financial-reports (includes 2024-25 Annual Investment Report)

- Facts at a Glance FY 2024–25: https://www.calpers.ca.gov/documents/facts-investments/download?inline

BlackRock TCP Capital (TCPC) Filings & Disclosures:

- IR / SEC Filings: https://tcpcapital.com/investor-relations/financials/sec-filings/default.aspx (includes May 2026 filings)

- Q1 2026 Results: https://tcpcapital.com/investor-relations/press-releases/press-release-details/2026/BlackRock-TCP-Capital-Corp--Announces-First-Quarter-2026-Financial-Results-Including-Net-Investment-Income-of-0-22-Per-Share-Declares-a-Second-Quarter-Dividend-of-0-17-Per-Share/default.aspx (May 7, 2026)

For full 10-Q/10-K or other SEC documents, search directly on https://www.sec.gov/edgar by company CIK or ticker around the relevant April–June 2026 dates. Many IR sites host the complete packs (press release + presentation + supplement + 10-Q).